ASIC puts directors, lead managers and corporate advisers of mining and exploration companies on notice

22 January 2020

The Australian Securities and Investments Commission (ASIC) has put directors, lead managers and corporate advisers of mining and exploration companies on notice of concerns regarding the multi-faceted role that lead managers and other promoters may play in the IPO process.

The mining and exploration industry represents over 25% of all ASX-listed entities. It accounted for more than 35% of all initial public offers (IPOs) during 2018 and, as at 1 August 2019, had a combined market capitalisation of over A$300 billion. Drawing upon their compulsory information-gathering powers, ASIC undertook a detailed review of a “sample” of 17 mining IPOs, occurring between 1 October 2016 and 30 September 2018, focusing on transactions raising less than A$20 million.

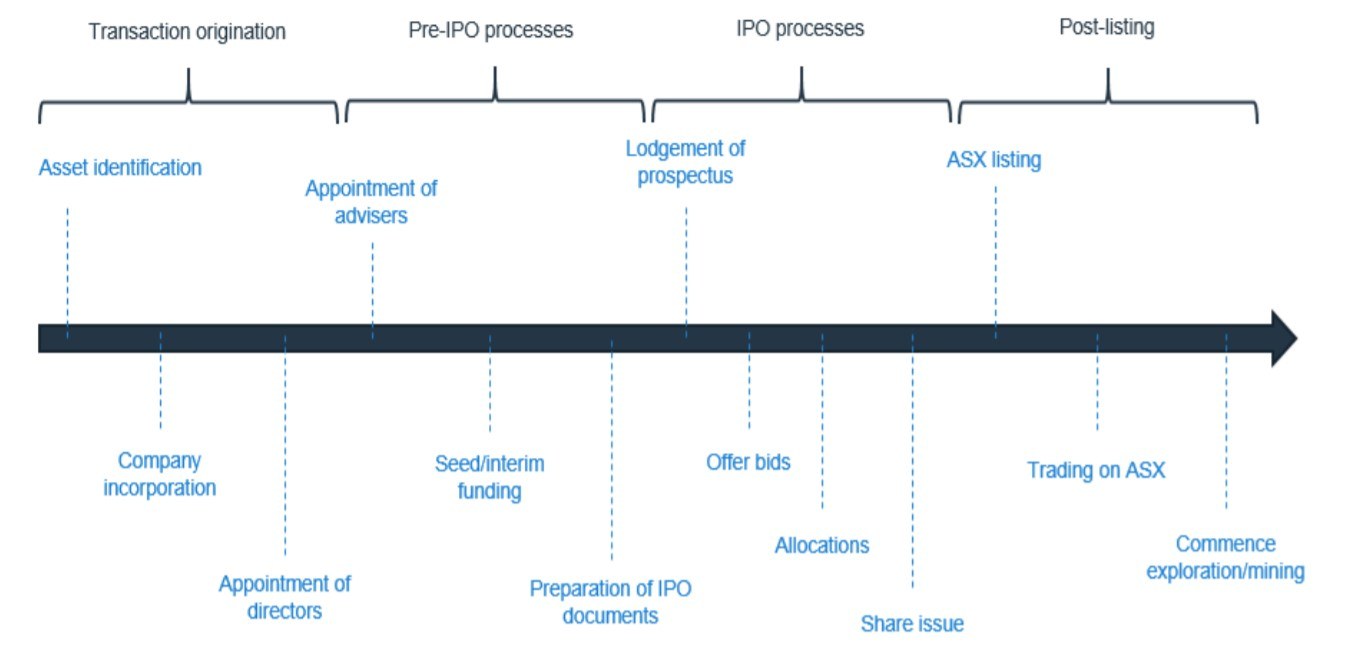

In a report released in late 2019 – Report 641 An inside look at mining and exploration initial public offers – ASIC flagged a number of concerns arising throughout all stages of the IPO process, from transaction origination through to on-market trading post-listing (depicted below – accessed from Report 641, page 8), with a particular focus on the conduct of lead managers.

ASIC’s concerns included the following:

- Professional advisors, including lead managers, are often heavily involved in all stages of the IPO process, including at times the inception of the company and transaction origination, and lead managers in particular have the potential to gain a disproportionate benefit through their direct involvement early on in the process.

- The significant potential for conflicts of interest to arise, particularly where the lead managers act for both the company as well as their investing clients or have representatives on the company’s board and/or prepare to provide ongoing advisory services in the post-IPO period.

- Lead managers having the potential to influence the register through preferential allocations to investors within their own networks, thereby being in a position to secure a greater level of influence over the company’s register and the composition of its board. ASIC’s review found that retail investors not associated with a lead manager may have limited access to these IPO investment opportunities.

- That the IPO process may place a greater focus on short term returns for a small pool of investors at the expense of investors with longer term investment horizons.

ASIC also expressed concerns around the use of less formal disclosure to investors, in the form of term sheets, investor presentations and other related communications, sometimes issued well in advance of (but with a view towards) an IPO.

‘Better Practice Recommendations’

In Report 641, ASIC put forward a comprehensive list of ‘better practice recommendations’ to assist companies, directors, lead managers and investors to reduce the risk of conflicts of interest, misconduct or regulatory harm associated with IPOs in the mining and exploration sector. The recommendations have been tailored to facilitate greater transparency and accountability, as well as to improve disclosure and independence, throughout the IPO process.

These recommendations include:

- Better disclosure of lead manager arrangements. A lead manager’s involvement in the transaction origination, and their interest in the entity being listed, should be clearly disclosed along with seed capital allocation and the amount/structure of fees and benefits payable in connection with the IPO. ASIC expects companies to have particular regard to the requirements of ASX’s Guidance Note 1 (Applying for Admission – ASX listings) in preparing for an IPO. Presentations and term sheets should not be used to make statements that could not be made in a prospectus.

- Conflicts of interests should be appropriately managed. Companies should have robust conflict management processes and procedures to manage conflicts of interests that may arise with the lead manager and other promoters. Lead managers should also ensure that appropriate conflict management procedures are adopted where they have multiple roles (such as lead manager, corporate adviser, investor adviser and/or shareholder) and that their mandates clearly articulate the scope of their services. Independent directors should be appointed as early as possible in the IPO process to enable them to closely scrutinise decisions made by transaction originators.

- Directors must assume greater control over the capital raising process. Directors should understand and, where appropriate, challenge the rationale behind the pricing and quantum of any seed funding sought (including the lead manager’s allocation strategy for seed capital) prior to an IPO. Directors should also be involved in setting the types of investors the company wishes to have apply for, and be allocated securities, under an IPO in order to better manage the company’s exposure to investors that may have short term investment horizons. Companies and lead managers are encouraged to heed the recommendations in the previously released ASIC Report 605 on equity raising allocations.

ASIC has said it will continue to monitor lead managers’ and companies’ conduct in connection with mining transactions (including practices that occur before and after lodgement of a prospectus), such that companies and lead managers who choose to ignore ASIC’s best practice recommendations do so at their peril.

Authors

Partner

Special Counsel

Tags

This publication is introductory in nature. Its content is current at the date of publication. It does not constitute legal advice and should not be relied upon as such. You should always obtain legal advice based on your specific circumstances before taking any action relating to matters covered by this publication. Some information may have been obtained from external sources, and we cannot guarantee the accuracy or currency of any such information.

Key Contact

Other Contacts